This week, the European Central Bank, Bank of England, and Federal Reserve are set to hold their meetings. What can we expect from the central banks, and can we anticipate a market reaction? Let's break it down in order.

The ECB is 99% likely to keep its monetary policy parameters unchanged, as recent events in the Middle East offer opportunities to resolve the conflict. As the past few weeks have shown, Tehran and Washington are not eager to resume war, which is already a positive sign. The negotiations are challenging and unofficial, but they are better than nothing. Thus, the ECB will likely adopt a wait-and-see position. If the situation in the Middle East does not worsen, there is hope that oil prices will not rise another 1.5-2 times. Consequently, inflation may stop accelerating, and tightening monetary policy may not be necessary.

The US central bank has not signaled any readiness to tighten policy in 2026. The most "hawkish" scenario the FOMC is prepared to implement is not to lower rates this year. However, easing policy is out of the question, as U.S. inflation accelerated by 0.9% year-on-year in March. Therefore, the Fed's stance is likely to be: it is unwise to ease policy, but they cannot afford to tighten it either. Additionally, this will be the last meeting under Jerome Powell's leadership. It is unlikely that the FOMC committee will make drastic moves with a new chairman, Kevin Warsh, set to take over in just 2.5 weeks.

The BoE is also expected to decide to keep its monetary policy parameters unchanged. Currently, markets anticipate that all nine members of the MPC will vote to maintain interest rates. Since only the BoE publishes voting results, this information will help market participants gauge the central bank's true sentiment. It is worth noting that inflation in the UK accelerated by only 0.3% year-on-year in March, and core inflation even slowed. Consequently, the BoE is likely not in the best mood, but the March inflation rate suggests a weak inflation shock due to the war in the Middle East and oil shortages. In my opinion, the BoE is the least likely to raise rates.

Given all of the above, all three banks are likely to make neutral decisions, but the BoE will provide information on the MPC voting results, and we cannot know what rhetoric the central bank heads will adopt.

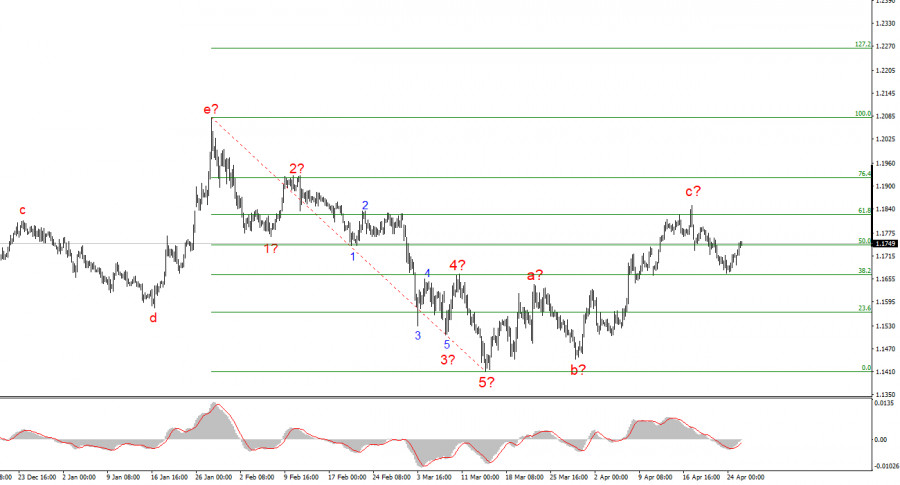

Based on my analysis of EUR/USD, I conclude that the instrument remains within an upward segment of the trend (as seen in the lower chart), while in the short term, it is within a corrective structure. The corrective wave set appears quite complete and may take on a more complex, extended form only if the geopolitical backdrop in the Middle East improves. Otherwise, I believe that a new downward wave set may begin from the current positions. We have observed a corrective wave; further movement will depend on the market's belief in a successful outcome of negotiations.

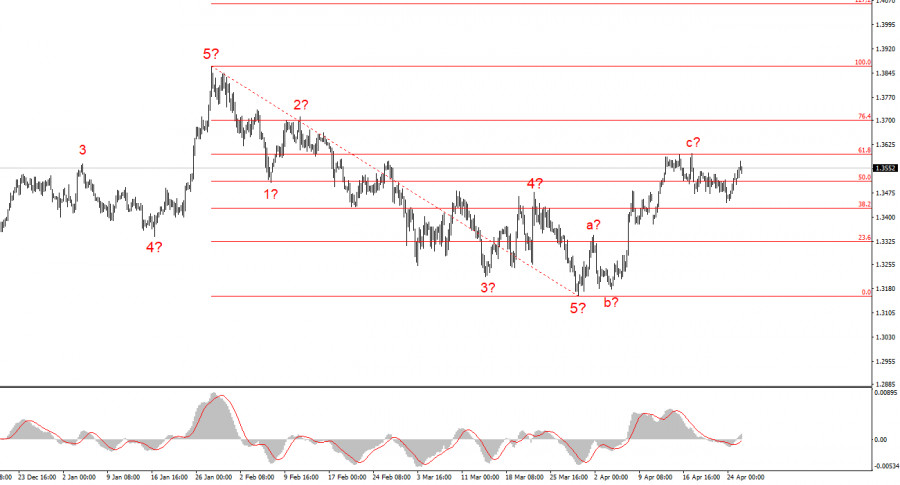

The wave structure of the GBP/USD instrument has become clearer over time, as I anticipated. We now see a clear three-wave upward structure on the charts, which may already be complete. If this is indeed the case, we can expect the formation of at least one descending wave (presumably wave d). The upward segment of the trend may take on a five-wave form, but for this to happen, the conflict in the Middle East needs to subside, not reignite. Therefore, the base scenario for the coming days is a decline to the 34th figure or slightly below. After that, everything will again depend on geopolitical factors.

SZYBKIE LINKI

ForexMart is authorized and regulated in various jurisdictions.

(Reg No.23071, IBC 2015) with a registered office at First Floor, SVG Teachers Co-operative Credit Union Limited Uptown Building, Corner of James and Middle Street, Kingstown, Saint Vincent and the Grenadines

Restricted Regions: the United States of America, North Korea, Sudan, Syria and some other regions.

Skontaktuj się z ForexMart

Skontaktuj się z ForexMart